Tuesday, June 27th, 2023

Today’s higher mortgage rates, inflationary pressures, and concerns about a potential recession have some people questioning: should I still buy a home this year? While it’s true this year has unique challenges for homebuyers, it’s important to think about the long-term benefits of homeownership when making your decision.

Consider this: if you know people who bought a home 5, 10, or even 30 years ago, you’re probably going to have a hard time finding someone who regrets their decision. Why is that? The reason is tied to how home values grow with time and how, by extension, that grows your own wealth. That may be why, in a recent Fannie Mae survey, 70% of respondents say they believe buying a home is a safe investment.

Here’s a look at how just the home price appreciation piece can really add up over the years.

Home Price Growth over Time

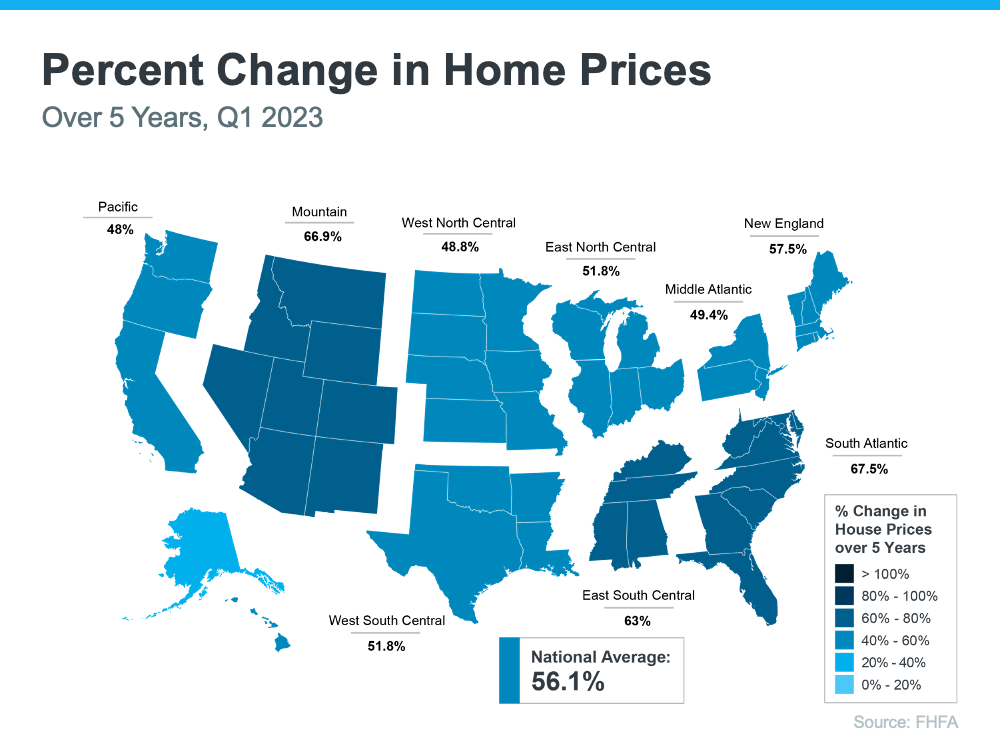

The map below uses data from the Federal Housing Finance Agency (FHFA) to show just how noteworthy price gains have been over the last five years. And, since home prices vary by area, the map is broken out regionally to help convey larger market trends.

If you look at the percent change in home prices, you can see home prices grew on average by just over 56% nationwide over a five-year period.

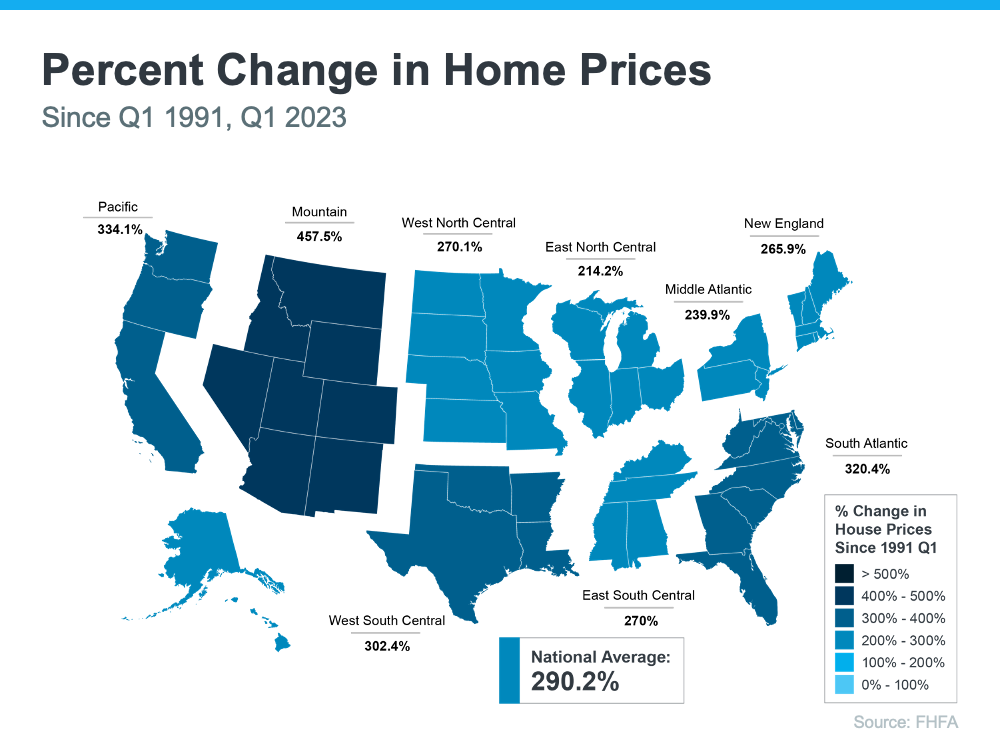

Some regions are slightly above or below that average, but overall, home prices gained solid ground in a short time. And if you expand that time frame even more, the benefit of homeownership and the drastic gains homeowners made over the years become even clearer (see map below):

The second map shows, nationwide, home prices appreciated by an average of over 290% over a roughly 30-year span.

This nationwide average tells you the typical homeowner who bought a house 30 years ago saw their home almost triple in value over that time. That’s a key factor in why so many homeowners who bought their homes years ago are still happy with their decision.

And while you may have heard talk in late 2022 that home prices would crash, it didn’t happen. Even though home prices have moderated from the record peak we saw during the ‘unicorn’ years, prices are already rebounding in many areas today. That means, in most markets, your home should grow in value over the next year.

The alternative to buying a home is renting, and rental prices have been climbing for decades. So why rent and deal with annual lease hikes for no long-term financial benefit? Instead, consider buying a home.

Bottom Line

If you’re questioning if it still makes sense to buy a home today, remember the incredible long-term benefits of homeownership. If you’re ready to start the conversation, reach out to a real estate professional today.

Friday, June 23rd, 2023

![Homeownership Helps Protect You from Inflation [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230622/Homeownership-Helps-Protect-You-From-Inflation-KCM-Share.png)

Some Highlights

- Wondering if it makes sense to buy a home today even when inflation is high? When other costs go up due to inflation, buying a home helps you keep your monthly housing expense steady.

- Rents typically increase with inflation. Maybe that’s why, according to a recent survey, 65.1% of landlords say they plan to raise the rent of at least one of their properties within the next 12 months.

- Especially when inflation is up, having a stable housing payment can be helpful. Connect with a local real estate agent so you can learn more and start your journey to owning a home today.

Thursday, June 22nd, 2023

If you’re thinking about buying a home, you should know your credit score’s a critical piece of the puzzle when it comes to qualifying for a home loan. Lenders review your credit to assess your ability to make payments on time, to pay back debts, and more. It’s also a factor that helps determine your mortgage rate. An article from Bankrate explains:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

This means your credit score may feel even more important to your homebuying plans right now since mortgage rates are a key factor in affordability, especially today. According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 765. But, that doesn’t mean your credit score has to be perfect. An article from Business Insider explains generally how your FICO score range can make an impact:

“. . . you don't need a perfect credit score to buy a house. . . . Aiming to get your credit score in the ‘Good’ range (670 to 739) would be a great start towards qualifying for a mortgage. But if you're wanting to qualify for the lowest rates, try to get your score within the ‘Very Good’ range (740 to 799).”

Working with a trusted lender’s the best way to get more information on how your credit score could factor into your home loan and the mortgage rate you’re able to get. As FICO says:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single "cutoff score" used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”

If you’re looking for ways to improve your score, Experian highlights some things you may want to focus on:

- Your Payment History: Late payments can have a negative impact by dropping your score. Focus on making payments on time and paying any existing late charges quickly.

- Your Debt Amount (relative to your credit limits): When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible.

- Credit Applications: If you’re looking to buy, don’t apply for other credit. When you apply for new credit, it could result in a hard inquiry on your credit that drops your score.

When you’re ready to start the homebuying process, a lender will be able to assess which range your score falls in and tell you more about the specifics for each loan type.

Bottom Line

With affordability challenges today, prioritizing ways you can have a positive impact on your credit score could help you get a better mortgage rate. If you want to learn more, connect with a trusted lender.

Tuesday, June 20th, 2023

The National Association of Realtors (NAR) will release its latest Existing Home Sales (EHS) report later this week. This monthly report provides information on the sales volume and price trend for previously owned homes. In the upcoming release, it’ll likely say home prices are down. This may feel a bit confusing, especially if you’ve been following along and seeing the blogs saying that home prices have bottomed out and turned a corner.

So, why will this likely say home prices are falling when so many other price reports say they’re going back up? It all depends on the methodology of each report. NAR reports on the median sales price, while some other sources use repeat sales prices. Here’s how those approaches differ.

The Center for Real Estate Studies at Wichita State University explains median prices like this:

“The median sale price measures the ‘middle’ price of homes that sold, meaning that half of the homes sold for a higher price and half sold for less . . . For example, if more lower-priced homes have sold recently, the median sale price would decline (because the “middle” home is now a lower-priced home), even if the value of each individual home is rising.”

Investopedia helps define what a repeat sales approach means:

“Repeat-sales methods calculate changes in home prices based on sales of the same property, thereby avoiding the problem of trying to account for price differences in homes with varying characteristics.”

The Challenge with the Median Sales Price Today

As the quotes above say, the approaches can tell different stories. That’s why median price data (like EHS) may say prices are down, even though the vast majority of the repeat sales reports show prices are appreciating again.

Bill McBride, Author of the Calculated Risk blog, sums the difference up like this:

“Median prices are distorted by the mix and repeat sales indexes like Case-Shiller and FHFA are probably better for measuring prices.”

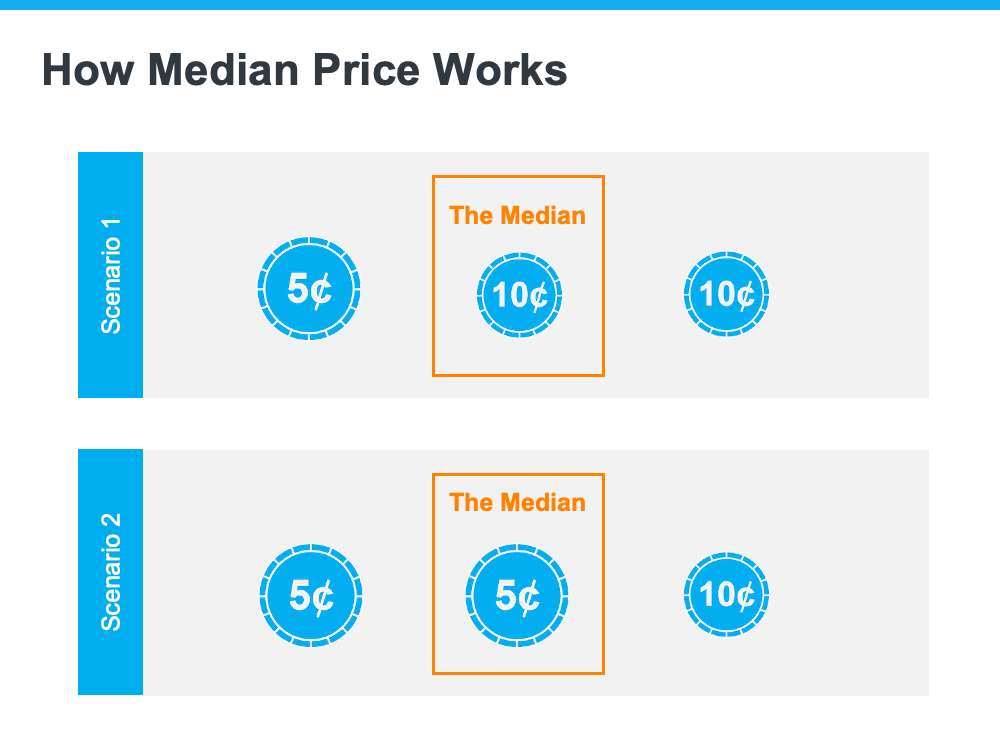

To drive this point home, here’s a simple explanation of median value (see visual below). Let’s say you have three coins in your pocket, and you decide to line them up according to their value from low to high. If you have one nickel and two dimes, the median value (the middle one) is 10 cents. If you have two nickels and one dime, the median value is now five cents.

In both cases, a nickel is still worth five cents and a dime is still worth 10 cents. The value of each coin didn’t change.

That’s why using the median home price as a gauge of what’s happening with home values isn’t worthwhile right now. Most buyers look at home prices as a starting point to determine if they match their budgets. But, most people buy homes based on the monthly mortgage payment they can afford, not just the price of the house. When mortgage rates are higher, you may have to buy a less expensive home to keep your monthly housing expense affordable. A greater number of ‘less-expensive’ houses are selling right now for this exact reason, and that’s causing the median price to decline. But that doesn’t mean any single house lost value.

When you see the stories in the media that prices are falling later this week, remember the coins. Just because the median price changes, it doesn’t mean home prices are falling. What it means is the mix of homes being sold is being impacted by affordability and current mortgage rates.

Bottom Line

For a more in-depth understanding of home price trends and reports, reach out to a local real estate professional.

Monday, June 19th, 2023

If you're planning to buy your first home, then you're probably focused on saving for all the costs involved in such a big purchase. One of the expenses that may be at the top of your mind is your down payment. If you’re intimidated by how much you need to save for that, it may be because you believe you must put 20% down. That doesn’t necessarily have to be the case. As the National Association of Realtors (NAR) notes:

“One of the biggest misconceptions among housing consumers is what the typical down payment is and what amount is needed to enter homeownership.”

And a recent Freddie Mac survey finds:

“. . . nearly a third of prospective homebuyers think they need a down payment of 20% or more to buy a home. This myth remains one of the largest perceived barriers to achieving homeownership.”

Here’s the good news. Unless specified by your loan type or lender, it’s typically not required to put 20% down. This means you could be closer to your homebuying dream than you realize.

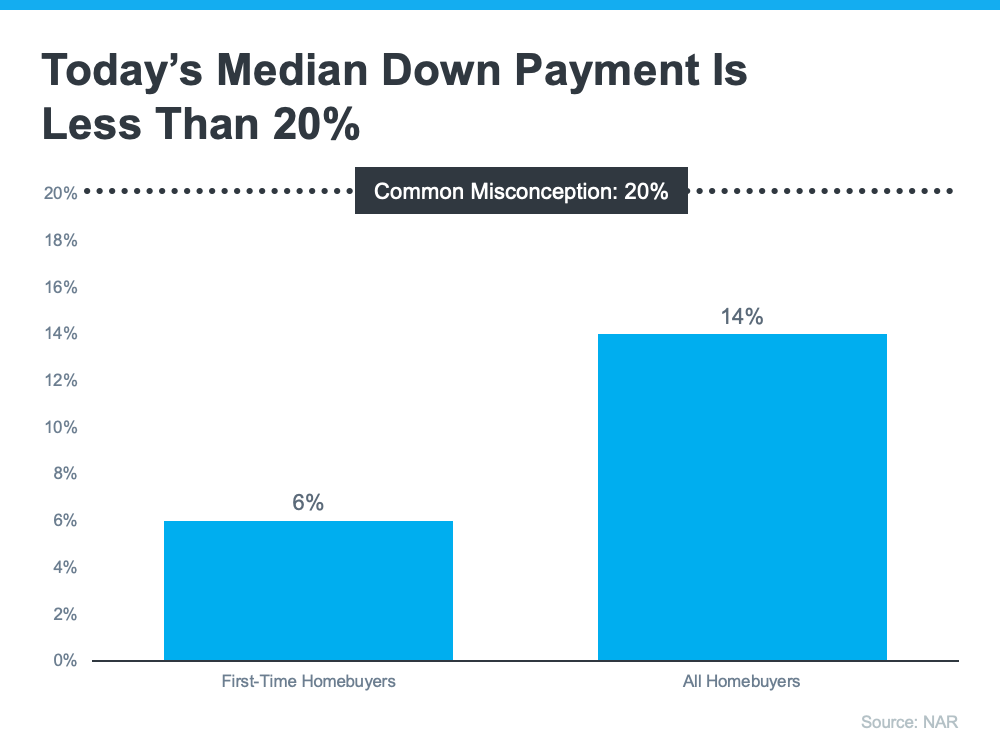

According to NAR, the median down payment hasn’t been over 20% since 2005. In fact, the median down payment for all homebuyers today is only 14%. And it’s even lower for first-time homebuyers at just 6% (see graph below):

What does this mean for you? It means you may not need to save as much as you originally thought.

Learn About Options That Can Help You Toward Your Goal

And it’s not just how much you need for your down payment that isn’t clear. There are also misconceptions about down payment assistance programs. For starters, many people believe there’s only assistance available for first-time homebuyers. While first-time buyers have many options to explore, repeat buyers have some, too.

According to Down Payment Resource, there are over 2,000 homebuyer assistance programs in the U.S., and the majority are intended to help with down payments. That same resource goes on to say:

“You don’t have to be a first-time buyer. Over 38% of all programs are for repeat homebuyers who have owned a home in the last 3 years.”

Plus, there are even loan types, like FHA loans with down payments as low as 3.5% as well as options like VA loans and USDA loans with no down payment requirements for qualified applicants.

If you’re interested in learning more about down payment assistance programs, information is available through sites like Down Payment Resource. Then, partner with a trusted lender to learn what you qualify for on your homebuying journey.

Bottom Line

Remember, a 20% down payment isn’t always required. If you want to purchase a home this year, reach out to a trusted real estate professional to start the conversation about your homebuying goals.

Friday, June 16th, 2023

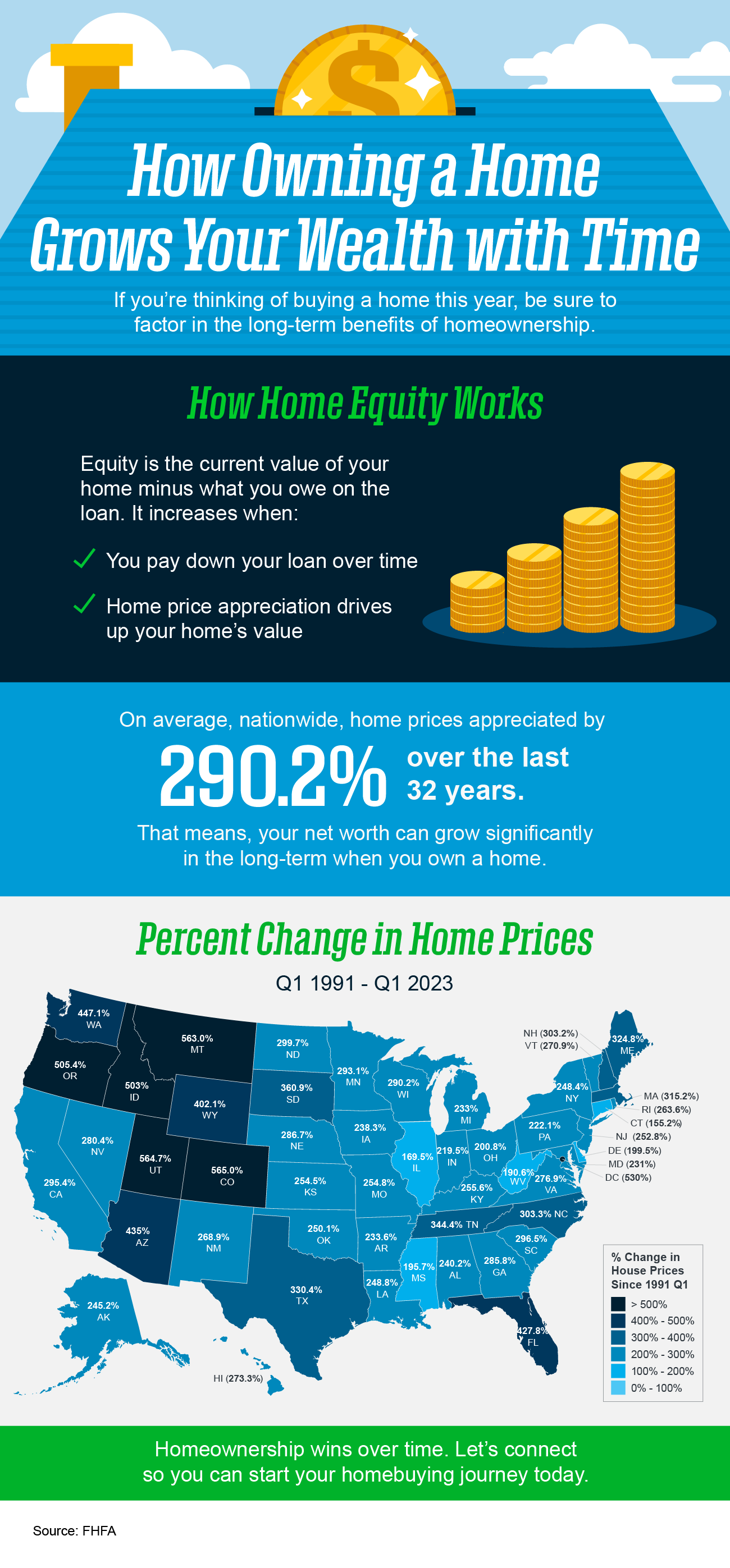

![How Owning a Home Grows Your Wealth with Time [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230615/How-Owning-a-Home-Grows-Your-Wealth-with-Time-KCM-Share.png)

Some Highlights

- If you’re thinking of buying a home this year, be sure to factor in the long-term benefits of homeownership.

- Over time, homeownership allows you to build equity. On average, nationwide home prices appreciated by 290.2% over the last 32 years.

- That means your net worth can grow significantly in the long term when you own a home. Reach out to a real estate professional so you can start your homebuying journey today.

Thursday, June 15th, 2023

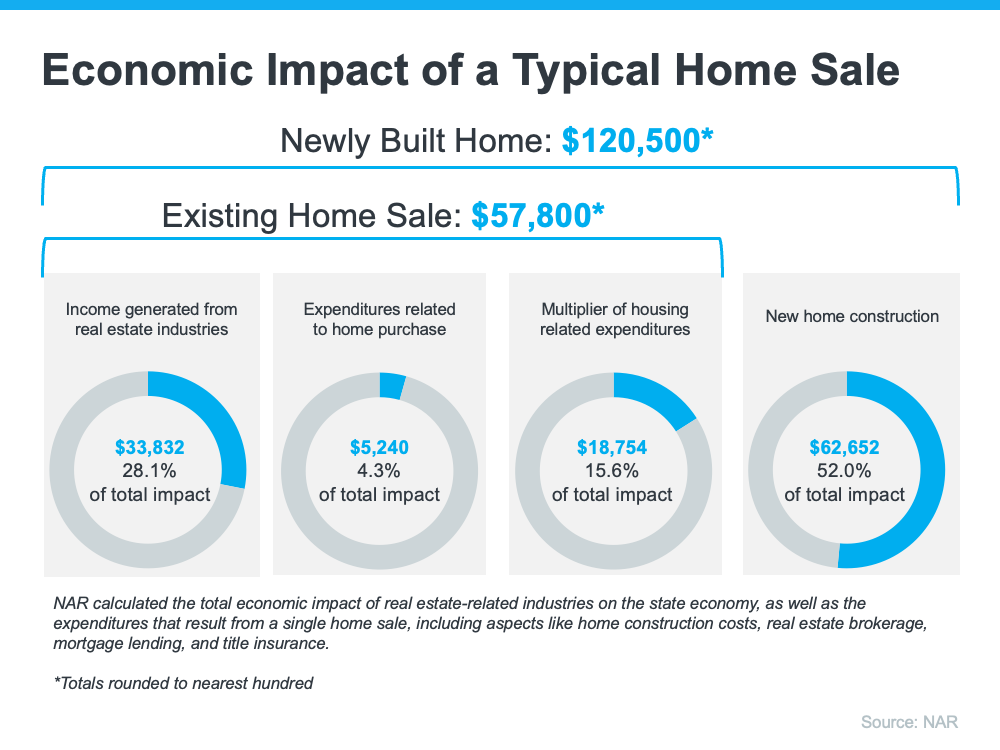

If you're thinking about buying or selling a house, it's important to know that it doesn't just affect your life, but also your community.

The National Association of Realtors (NAR) releases a report every year to show how much economic activity is generated by home sales. The chart below illustrates that impact:

As the visual shows, when a house is sold, it can make a big difference in the local economy. The impact comes largely from the workers required to build, update, and buy and sell homes. Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), explains how the housing industry adds jobs to a community:

“The economic impact means housing is a significant job creator. In fact, for every single-family home built, enough economic activity is generated to sustain three full-time jobs for a year, per NAHB research. . . . And one job for every $100,000 in remodeling spending.”

Housing being a major job creator makes sense when you consider there are many different industries involved in the process. A recent article from Fortune notes housing activity could have a more robust impact than you think due to the many ways it’s tied to the economy:

“Housing has three direct linkages to economic activity (GDP): the construction of new homes, the remodeling of existing homes, and that of housing transactions. . . . consider the activity associated with home sales – think broker fees, lawyers, etc. – which are a sizable contributor to housing’s GDP footprint.”

When you buy or sell a home, you work with a team of professionals, including contractors, specialists, lawyers, and city officials. Each person plays a role in making the transaction happen.

So, when you make a move in the housing market, you're not just meeting your own needs, you're also making a positive impact on the community. Knowing this can give you a sense of empowerment as you make your decision this year.

Bottom Line

Each and every home sale is important for the local economy. If you’re ready to move, reach out to a trusted real estate agent. It won’t just change your life – it’ll also have a strong positive effect on the whole community.

Wednesday, June 14th, 2023

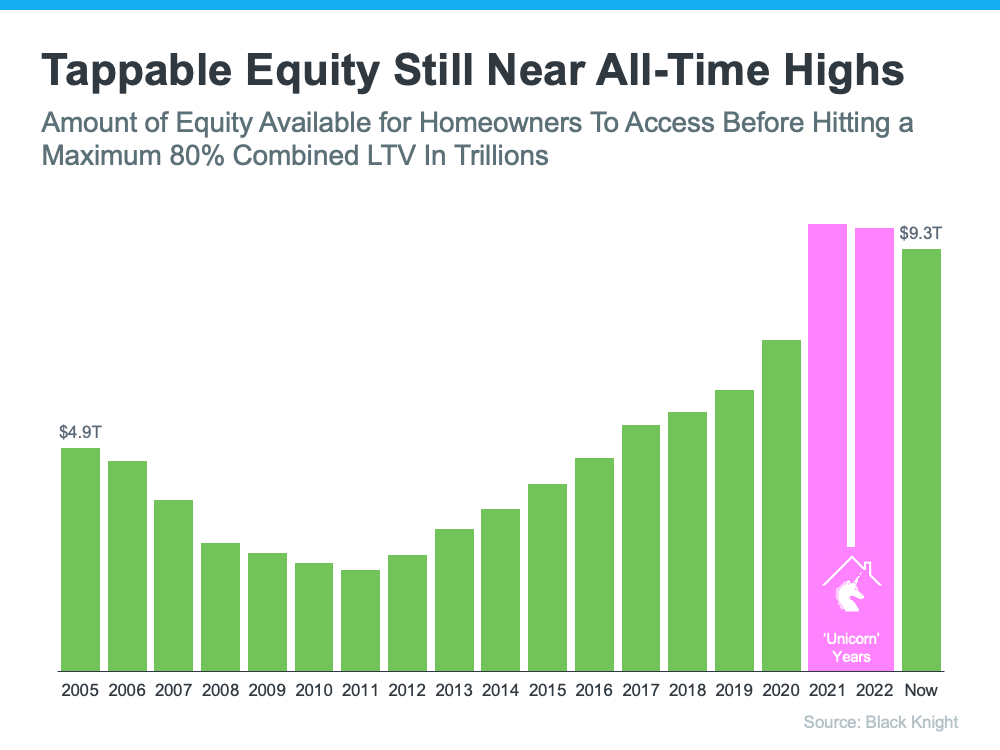

You may see media coverage talking about a drop in homeowner equity. What’s important to understand is that equity is tied closely to home values. So, when home prices appreciate, you can expect equity to grow. And when home prices decline, equity does too. Here’s how this has played out recently.

Home prices rose rapidly during the ‘unicorn’ years. That gave homeowners a considerable equity boost. But those ‘unicorn’ years couldn’t last forever. The market had to moderate at some point, and that’s what we saw last fall and winter.

As home prices dropped slightly in the back half of 2022, equity was impacted. Based on the most recent report from CoreLogic, there was a 0.7% dip in homeowner equity over the last year. However, the headlines reporting on that change aren’t painting the whole picture. The reality is, while home price depreciation during the second half of last year caused equity to drop, the data shows homeowners still have near record amounts of equity.

The graph below helps illustrate this point by looking at the total amount of tappable equity in this country going all the way back to 2005. Tappable equity is the amount of equity available for homeowners to access before hitting a maximum 80% loan-to-value ratio (LTV). As the data shows, there was a significant equity boost during the ‘unicorn’ years as home prices rapidly appreciated (see the pink in the graph below).

But here’s what’s key to realize – even though there’s been a small dip, total homeowner equity is still much higher than it was before the ‘unicorn’ years.

And there’s more good news. Recent home price reports show the worst home price declines are behind us, and prices have started to go up again. As Selma Hepp, Chief Economist at CoreLogic, explains:

“Home equity trends closely follow home price changes. As a result, while the average amount of equity declined from a year ago, it increased from the fourth quarter of 2022, as monthly home prices growth accelerated in early 2023.”

The last part of that quote is particularly important and is the piece of the puzzle the news is leaving out. To further emphasize the positive turn we’re already seeing, experts say home prices are forecast to appreciate at a more normal rate over the next year. In the same report, Hepp puts it this way:

“The average U.S. homeowner now has more than $274,000 in equity – up significantly from $182,000 before the pandemic. Also, while homeowners in some areas of the country who bought a property last spring have no equity as a result of price losses, forecasted home price appreciation over the next year should help many borrowers regain some of that lost equity.”

And even though Odeta Kushi, Deputy Chief Economist at First American, references a slightly different number, Kushi further validates the fact that homeowners have a lot of equity right now:

“Homeowners today have an average of $302,000 in equity in their homes.”

That means if you’ve owned your home for a few years, you likely still have way more equity than you did before the ‘unicorn’ years. And if you’ve owned your home for a year or less, the forecast for more typical price appreciation over the next year should mean your equity is already on the way back up.

Bottom Line

Context is everything when looking at headlines. While homeowner equity dropped some from last year, it’s still near all-time highs. Reach out to a trusted real estate professional so you can get the answers you deserve from an expert who’s there to help as you plan your move this year.

Tuesday, March 20th, 2018

We frequently get questions from clients who are taking on decorating and remodeling projects and want to ensure their dollars are invested wisely.

Which looks will last for years to come, and which ones will feel dated quickly? What colors and styles are most popular among buyers in our area? How can I add the most value to my home?

So we’ve rounded up some of the hottest trends in home design to help guide you through the process. Whether you’ve planned a simple refresh or a full-scale renovation, making smart and informed design choices will help you maximize your return on investment … and minimize the chance of “remodeler’s remorse” down the road.

WHAT’S HOT NOW

While 2017 was all about millennial pink, brass fixtures and bright white kitchens, this year we expect to see a move toward warmer, cozier elements throughout the home.

1. Warm Colors

A cool color scheme has dominated home design in recent years, but this year warm neutrals like brown and tan are back, along with rich jewel tones. While the pastel craze of last year is still hanging on, expect to see alternative color palettes featuring deep, saturated shades of red, yellow, green and navy. Grey will remain popular, but in warmer tones, often referred to as “greige.”

2. Cozy Elements

Along with warmer colors, we can expect to see a shift from stark, modern design to cozier looks. Velvet upholstery, woven textures and natural elements, like wood and stone, will heat things up this year.

3. Mixed Metals

It used to be considered gauche to mix finishes, however the look of mixed metals will be very big in 2018. Brass will continue to trend, along with matte black and classics like polished chrome and brushed nickel.

4. Bold Patterns

Expect to see a lot of bright, bold patterns in the form of geometric shapes and graphic floral prints. These will be featured on everything from furniture to throw pillows to tile.

5. Natural Elements

Look for the use of natural elements throughout the home, including wood, stone, plants, flowers and grass. Botanical patterns will also be seen in prints, wallpaper and upholstery. Concrete accents will complement these additions in an effort to bring the essence of the outdoors inside the home.

6. Feature Walls

Also called an accent wall, a feature wall is one that exhibits a different color or design than the other walls in the room. Expect to see an increased use of feature walls showcasing rich paint colors, bold patterned wallpaper, and textures brought in through millwork and shiplap.

7. Statement Lighting

Lighting will take center stage with distinctive fixtures, including local artisan and vintage pendants and chandeliers. And smart lighting technology will enable homeowners to customize their lighting experience based on time of day, activity and mood.

8. Hardwood Floors

Hardwood floors will continue to dominate the market. The trend is toward either very dark stains paired with light-colored walls or light stains with darker walls. Greyish tones will remain popular, as will matte finishes, which are easier to maintain than high gloss. Expect to see frequent use of wider and longer wood planks, as well as distressed and wire-brushed finishes, which add texture and dimension.

9. Smart Homes

Everything is getting “smarter” in homes, from locks and lights to thermostats and appliances. And with devices like Google Home and Amazon Alexa, you can control many of these with voice activation from a central hub. We will see continued integration of and advancements in smart-home technology in 2018.

KITCHEN TRENDS

While white kitchens will remain popular in 2018, expect to see more color this year in everything from cabinets to tile to appliances.

1. Two-toned Cabinets

Two-toned cabinets are quickly overtaking the white-on-white look that has dominated kitchen design for the past few years. While white remains a classic, grey and bleached-wood cabinet variations are surging in popularity, along with darker neutrals like navy and green.

2. Quartz Countertops

Granite reigned as the top countertop choice for many years, but quartz is now king. It’s highly durable, low-maintenance and comes in a wide variety of styles and colors. It’s also heat resistant, scratch resistant and non-porous (unlike granite and marble) so it doesn’t need to be sealed.

3. Bold Backsplashes

After years of dominating backsplash design, the white subway tile is officially on its way out. Expect to see it replaced with more elaborate shapes, patterns, colors and textures. Tile that mimics the appearance of wood, concrete and wallpaper is also gaining in popularity.

4. Statement Sinks

While stainless steel and white porcelain are always safe bets, the trend is moving toward sinks that make more of a statement. Look for unexpected pops of color and materials like natural stone and copper. Touch-free faucets are expected to gain favor with homeowners this year, too.

5. Brass is (Still) Back

Brass fixtures came back in a big way over the past couple of years and will continue to be a popular choice in 2018 along with matte black, black nickel, polished chrome and brushed nickel. Missing from the list? Rose gold, which is decidedly “out” this year.

6. Multi-purpose Islands

Kitchen islands have evolved from simple prep-stations into the “workhorse” of the kitchen. Many feature sinks, built-in appliances and under-counter storage while also serving as a casual dining area. They have become the focal point of the kitchen, and we expect to see more of them in 2018 and beyond.

7. Black Stainless Steel

Black stainless steel is the hot new finish option for appliances, and it’s hitting the market in a big way. It offers a cutting-edge look and is easier to keep clean than traditional stainless steel. However, it’s harder to match finishes amongst different brands, so it’s probably only feasible as part of a complete appliance package.

8. Appliance Garages

Appliance garages are counter-level compartments designed to house small appliances like blenders, toasters and stand mixers. They make it convenient to have these items readily accessible, without the look of a cluttered counter.

BATH TRENDS

Expect to see many of the same kitchen design preferences carry over into bathrooms this year, including two-tone cabinets, quartz countertops and brass fixtures.

1. Neutral Tones

Neutral shades will continue to dominate in the master bathroom as homeowners seek a soothing and relaxing retreat atmosphere. But expect to see more options than just white. Shades of brown, grey, blue, green and tan will help to warm things up.

2. Natural Elements

Natural materials are particularly hot right now in bathroom design. This includes the use of wood and stone on walls, cabinets, counters and backsplashes, as well as the incorporation of botanical design elements.

3. Large Tiles

We expect to see a lot more large and slab-sized tiles in bathrooms, which have less grout so they are easier to clean and maintain. Wood-look porcelain tiles are also a favorite in wet areas, as they offer the warmth and rustic appeal of wood with the durability of tile.

4. Stone Sinks

Sinks will continue to be an area where homeowners like to exhibit creativity, and hand-carved stone sinks are especially fashionable right now. These may be more suited to powder rooms, where functionality isn’t as crucial.

5. Freestanding Tubs

There’s been a tub resurgence in bathroom design after years of preference for stand-alone showers. Modern tastes are gravitating toward freestanding tubs that serve as a showpiece for the bathroom.

6. Smart Features

Smart technology has entered the bathroom with the addition of features like wireless shower speakers and high-tech toilets, as well as digital shower controls that automatically adjust to your preferences in temperature and spray intensity.

OUR ADVICE

Style trends come and go, so don’t invest in the latest look unless you love it. That said, highly-personalized or outdated style choices can limit the appeal of your property for resale.

For major renovation projects, it’s always a good idea to stick to neutral colors and classic styles. It will give your remodel longevity and appeal to the greatest number of buyers when it comes time to sell. It will also give you flexibility to update your look in a few years without a total overhaul. Use non-permanent fixtures – like paint, furniture and accent pieces – to personalize the space and incorporate trendier choices.

If you’d like advice on a specific remodelling or design project, give us a call! We’re happy to offer our insights and suggestions on how to maximize your return on investment and recommend local shops and service providers who may be able to assist you.

Sources:

- Country Living –

http://www.countryliving.com/home-design/decorating-ideas/g3988/kitchen-trends

- Elle Decor –

http://www.elledecor.com/design-decorate/trends/g14486069/kitchen-trends-2018/

- Gates Interior Design –

https://gatesinteriordesign.com/hottest-interior-design-trends-for-2018/

https://gatesinteriordesign.com/biggest-kitchen-bath-trends-for-2018/

- com –

http://www.hgtv.com/design/rooms/kitchens/17-top-kitchen-design-trends-pictures

- House Beautiful –

http://www.housebeautiful.com/room-decorating/kitchens/g2664/kitchen-trends/

http://www.housebeautiful.com/design-inspiration/g13938283/2018-decor-trends/

http://www.housebeautiful.com/design-inspiration/g13820501/best-and-worst-decor-trends-from-2017/

- Houzz –

https://www.houzz.com/ideabooks/93399913/list/interior-design-trends-expected-to-take-hold-in-2018

- Huffington Post – http://www.huffingtonpost.com.au/2017/09/25/the-kitchen-and-dining-trends-to-look-out-for-in-2018_a_23222693/

- Kitchen and Bath Design News –

http://www.kitchenbathdesign.com/123995/year-end-look-and-new-trends-for-2018/

- com –

https://www.msn.com/en-us/lifestyle/home-and-garden/12-flooring-trends-for-2018/ss-AAtp7QA

- com –

https://www.realtor.com/advice/home-improvement/interior-design-trends-to-ditch-2018/

https://www.realtor.com/advice/home-improvement/hottest-interior-design-decor-trends-2018/?is_wp_site=1

- Realty Times – http://realtytimes.com/advicefromagents/item/1007993-kitchen-design-trends-in-2018?rtmpage=MattLawler

- Sebring Design Build –

https://sebringdesignbuild.com/top-trends-in-bathroom-design/

- The Flooring Girl –

http://theflooringgirl.com/hardwood-flooring/hardwood-flooring-trends-2018/

- Vogue –

https://www.vogue.com/article/interior-design-trends-according-to-expert-designers-decorators